Economic Observer Follow

2026-04-19 19:33

![]()

The tourism boom in 2025 has boosted the performance recovery of airlines.

In the past year, from the peak of "visiting relatives and traveling" during the Spring Festival, the popularity of travel during the May Day and Dragon Boat Festival holidays, to the flourishing of summer parent-child and study tours, as well as the cross provincial long-distance travel trend during the National Day and Mid Autumn Festival holidays, the passenger load factor of airlines has increased. According to data from the Civil Aviation Administration of China, by 2025, the entire civil aviation industry in China will have transported 770 million passengers, a year-on-year increase of 5.5%.

According to the report of the 2026 National Civil Aviation Work Conference, China's total aviation population has exceeded 500 million, making it the world's largest aviation population country.

The airline is gradually getting rid of the shadow of losses.

China Southern Airlines (600029.SH/1055HK, hereinafter referred to as "China Southern Airlines") has made its first profit in six years, breaking the continuous losses of the three major airlines after the epidemic. Eastern Airlines (600115.SH/0670.HK, hereinafter referred to as "Eastern Airlines") and Air China (601111.SH/0753.HK, hereinafter referred to as "Air China") are still operating at a loss, mainly due to an accounting treatment that has improved their actual operating conditions.

In addition to the three major airlines, the revenue and net profit of private airlines are also growing. Spring Airlines (601021. SH) remains the most profitable airline in China, and Cathay Pacific Airways (0293. HK) located in Hong Kong has also achieved dual growth in revenue and net profit.

Wu Chenyue, a transportation analyst at Huachuang Securities, said that 2025 is the year when the industry will move towards substantial improvement in performance. The key sign is that multiple companies have submitted reports of reducing or reversing losses: China Southern Airlines has achieved a turnaround; China Eastern Airlines has significantly reduced its losses, and its total profit has turned around; Air China's operating profit decreased by nearly 1.4 billion yuan; Hainan Airlines (600221. SH) and Huaxia Airlines (002928. SZ) also announced profits. Senior transportation and logistics industry management consultant Yu Zhanfu believes that in terms of scale, 2025 is the true year of comprehensive recovery for China's civil aviation in the post pandemic era.

Performance Restoration

The profit fluctuations of airlines are mainly affected by domestic and international macroeconomic situations, geopolitical conflicts, international crude oil prices, RMB exchange rates, major emergencies (such as epidemics, snow disasters, earthquakes, etc.), and other special events.

Before 2020, China's civil aviation industry had maintained profitability for 11 consecutive years; From 2020 to 2022, the industry has accumulated significant losses; It will not be until 2023 that the turning point of recovery will be reached. The 2023 Statistical Bulletin on the Development of the Civil Aviation Industry shows that airlines have achieved a significant reduction in losses of 164.4 billion yuan.

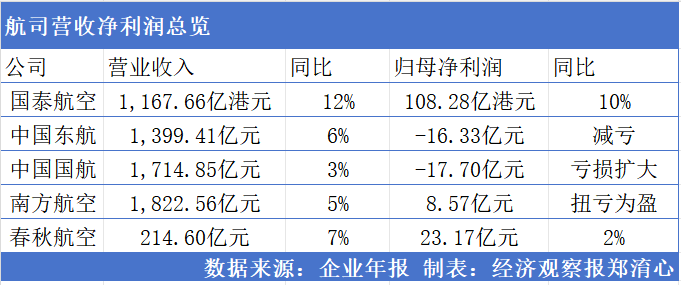

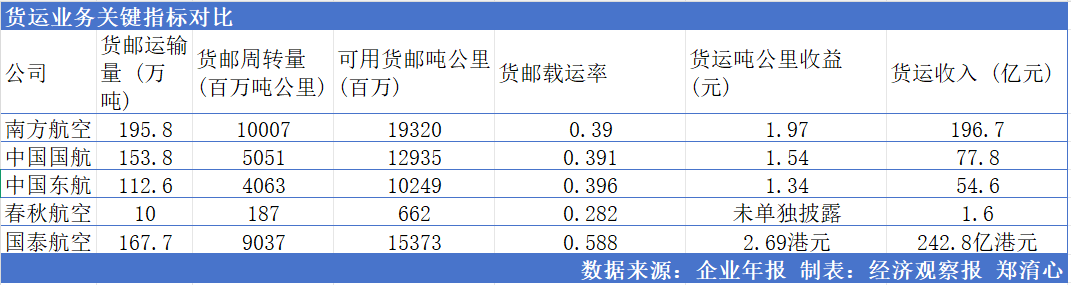

China Southern Airlines has become the first airline among the three major airlines to achieve profitability since the outbreak of the epidemic, with a total revenue of 182.252 billion yuan in 2025, a year-on-year increase of 4.61%; The net profit attributable to the parent company was 857 million yuan, turning losses into profits. According to the financial report, China Southern Airlines' profit this time mainly comes from its yet to be divested cargo division. China Southern Airlines Logistics achieved a net profit of 4.186 billion yuan, contributing approximately 3.575 billion yuan in net profit to China Southern Airlines based on its shareholding ratio.

China Eastern Airlines and Air China have previously listed their cargo segments separately. China Eastern Airlines Logistics (601156. SH) completed its A-share listing in June 2021. Air China (001391. SZ) was listed on the Shenzhen Stock Exchange in December 2024, becoming the largest A-share IPO of the year at that time. The road to listing of China Southern Airlines Logistics began in 2022. In February 2025, the latest announcement stated that based on the current market environment changes and in order to coordinate capital operation planning, after full communication and careful consideration, China Southern Airlines Logistics plans to withdraw its application for listing on the main board of the Shanghai Stock Exchange.

In terms of overall scale, the three major airlines achieved a total operating revenue of approximately 493.682 billion yuan, exceeding the level of the same period in 2019.

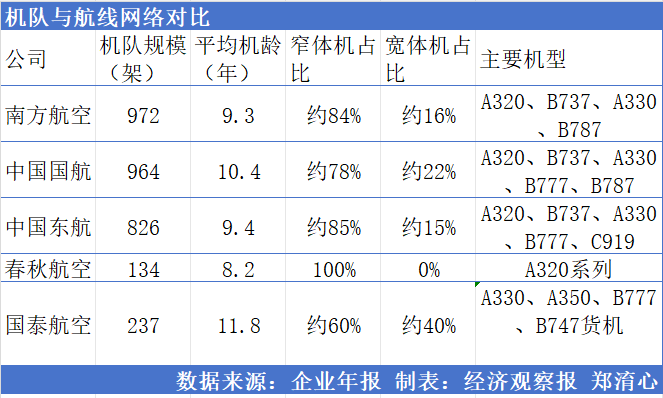

Wu Chenyue believes that the improvement of airline performance is mainly affected by three aspects. One is the increase in industry utilization, especially the increase in the utilization of wide body aircraft, which effectively dilutes costs. The second is the increase in passenger load factor, which contributes to seat kilometer revenue. By 2025, the overall passenger load factor of the industry will increase to over 85%, driven by the growth of demand resilience and low growth rate of supply. In 2025, the growth rate of each airline's fleet (referring to the total number of aircraft owned by an airline) will be relatively low (such as 3.7% for Air China, 2.7% for China Eastern Airlines, and 3.9% for Spring Airlines), and according to the announced plans for the next three years, the total growth rate of the three major airlines in 2026 will only be 2.4%. The third is the structural trend of demand, where the growth rate of international demand is significantly faster than that of domestic demand, which is conducive to driving overall turnover.

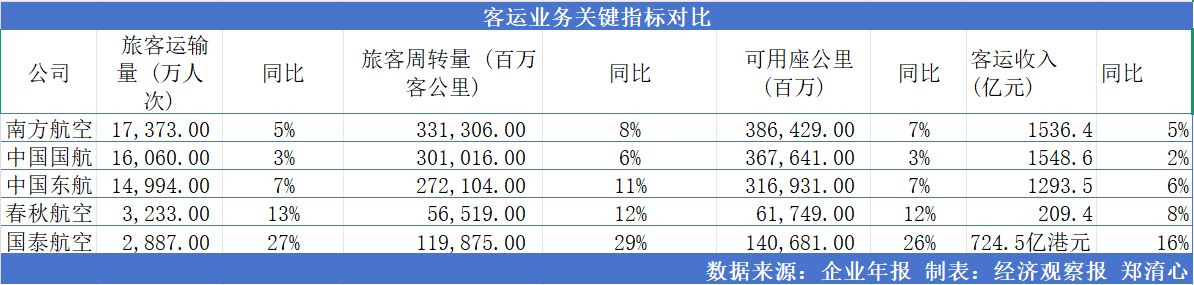

Comparing the key indicators of passenger transport business, it can be seen that the passenger transport volume and passenger revenue of each airline have both achieved growth.

But the performance of the three major airlines is also differentiated: except for the profitable China Southern Airlines, Air China's losses are expanding, while China Eastern Airlines' losses are decreasing. Air China achieved a revenue of 171.485 billion yuan, a year-on-year increase of 2.87%; The net loss attributable to the parent company was 1.77 billion yuan, with the loss expanding by 1.533 billion yuan. China Eastern Airlines achieved a revenue of 139.941 billion yuan, a year-on-year increase of 5.92%; The net loss attributable to the parent company was 1.633 billion yuan, a year-on-year decrease of 2.593 billion yuan.

From the perspective of operating profit, Air China's annual operating profit for 2025 decreased from -3.43 billion yuan to -2.05 billion yuan, narrowing the loss by approximately 1.38 billion yuan. However, the ultimate expansion of Air China's losses was the result of the one-time accounting impact of the reversal of deferred tax assets, combined with the drag of subsidiaries and the slow recovery of route structure.

Not only Air China, but also China Eastern Airlines has been affected by the one-time accounting impact of the reversal of deferred tax assets. Deferred tax assets are the recognition of future deductible temporary differences within the framework of accounting standards. During the epidemic, airlines accumulated a large amount of deferred tax assets due to huge losses. When the profit margin improves, according to the principle of prudence, if it is assessed that the future deductible amount is lower than the previously recognized level, it needs to be reversed, which is reflected as an increase in current income tax expenses, directly reducing the net profit attributable to the parent company.

By quarter, in the first three quarters of 2025, the three major airlines collectively turned losses around, with Air China, China Eastern Airlines, and China Southern Airlines achieving net profits attributable to their parent companies of 1.87 billion yuan, 2.103 billion yuan, and 2.307 billion yuan, respectively.

Both China Southern Airlines, which was the first to turn losses around, and Air China, which continued to record losses, were dragged down by the traditional off-season in the fourth quarter. In the fourth quarter, Air China had a net loss of 3.64 billion yuan, China Southern Airlines had a net loss of 1.45 billion yuan, and China Eastern Airlines had a net loss of 3.736 billion yuan.

Yu Zhanfu believes that what is more important than financial losses is the substantial repair of the main business's ability to generate revenue. The net cash flow generated from the annual operating activities of Air China reached 42.045 billion yuan, Eastern Airlines reached 37.941 billion yuan, and Southern Airlines reached 38.209 billion yuan. This means that the three major airlines hold sufficient cash flow and have the foundation to open up new routes, upgrade service facilities, and develop "aviation+" businesses.

At the same time, the losses of subsidiary airlines have also dragged down the performance of the three major airlines.

Among the 9 holding companies disclosed by Air China, only Beijing Aircraft Maintenance Engineering Co., Ltd. (Ameco), AVIC Finance, and Cathay Pacific Airways achieved profitability, while Shenzhen Airlines, Shandong Airlines Group, Beijing Airlines, Dalian Airlines, Inner Mongolia Airlines, and Macau Airlines did not achieve profitability.

Among the subsidiary airlines of China Southern Airlines, Shantou Airlines, Zhuhai Airlines, Guizhou Airlines, Chongqing Airlines, and Henan Airlines all incurred losses; But Xiamen Airlines achieved a profit of 779 million yuan, and China Southern Airlines Logistics achieved a profit of 3.575 billion yuan.

Among the subsidiaries of China Eastern Airlines, only United Airlines made a profit of 108 million yuan, while Jiangsu Airlines, Wuhan Airlines, Yunnan Airlines, and Shanghai Airlines all incurred losses.

Among private airlines, Spring Airlines remains the most profitable airline in mainland China, with a net profit attributable to its parent company of 2.317 billion yuan.

Yu Zhanfu said that Spring Airlines has built a moat with an extremely low-cost model, and its unit cost per available seat kilometer is the lowest in the industry, and its 91.5% passenger load factor is also the highest in the industry. In addition, Spring Airlines adopts a single aircraft model and a fleet of narrow body aircraft, reducing maintenance and operating costs and improving operational efficiency.

In addition, the accelerated recovery of inbound and outbound tourism has contributed considerable revenue to airlines. According to data from the Civil Aviation Administration of China, international flights will resume to over 90% of 2019 levels by 2025, and international passenger traffic will increase by 21.6% year-on-year. This directly drives the improvement of the airline's international business. China Eastern Airlines' international business revenue increased by 20.82% year-on-year, while Air China's international passenger revenue increased by 14.13% year-on-year. At the performance briefing, China Southern Airlines stated that benefiting from the continuous release of dividends from the demand for economic, trade, and tourism in Central Asia, the relevant routes will have good market support.

Efficiency improvement and cost challenges

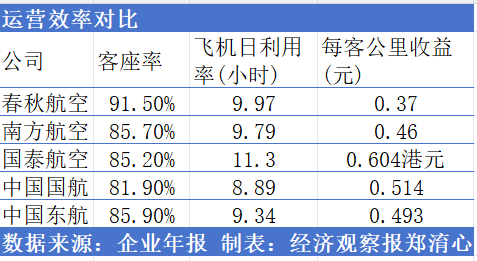

Passenger load factor is one of the key indicators to measure the operational efficiency of an airline. In 2025, the passenger load factors of Air China, China Eastern Airlines, and China Southern Airlines will be 81.88%, 85.86%, and 85.74%, respectively, an increase of 2 to 3 percentage points from the previous year, exceeding pre pandemic levels.

An industry analyst said that the difference in passenger load factor among the three major airlines is mainly related to the differences in network and fleet structure. Air China has the most wide body aircraft designed specifically for long haul routes among the three major airlines, with North America being one of its traditional advantage routes. However, the recovery rate of North American routes is relatively low, which has dragged down the efficiency of wide body aircraft. China Southern Airlines has a higher proportion of recovered routes in Southeast Asia and other regions. In addition, various airlines have different balance strategies between passenger load factor and ticket price, but according to the latest data, Air China has been adjusting its strategy, with a year-on-year increase in passenger load factor from January to March this year.

According to the financial report, in 2025, Air China's revenue per passenger kilometer is about 0.51 yuan, China Eastern Airlines' revenue per passenger kilometer is about 0.49 yuan, and China Southern Airlines' revenue per passenger kilometer is about 0.46 yuan, all with a decrease of about 4%. Against the backdrop of increased capacity investment and passenger load factor, unit revenue is declining.

Therefore, airlines need to keep planes flying longer in order to partially dilute costs. In terms of daily aircraft usage, Cathay Pacific ranks first, followed by Spring Airlines, and Air China ranks last.

Yu Zhanfu said that Cathay Pacific's high utilization rate is due to its efficient hub flight schedule, which refers to Cathay Pacific carefully designing its flight schedule to gather flights from all over the world in one "wave", allowing passengers to efficiently transfer and then have the same aircraft take off again in a short period of time, executing more flight segments. Spring Airlines maximizes aircraft utilization by extending flight schedules and reducing transit times, which is the key to cost dilution. However, the low utilization rate of Air China is partly due to its large wide body fleet, which operates on long-distance international routes with long single flight times but fewer daily takeoffs and landings, which lowers the average utilization rate.The cost of wide body aircraft is higher, and the direct way to improve their efficiency is to fly long international routes.

Wu Chenyue said that from the perspective of operational efficiency, the resumption of international routes is a win-win situation for airlines. It can not only improve the utilization rate of wide body aircraft, but also reduce the capacity investment in the domestic market and alleviate competitive pressure. The restoration of international routes has effectively revitalized the idle wide body aircraft assets of airlines, significantly improved operational efficiency, and solved the pain points of asset idle.

In the summer and autumn aviation seasons, the three major airlines are also intensifying their efforts in the international market.

In 2026, China Southern Airlines Group plans to add major routes including Xiamen Vientiane, Fuzhou Amsterdam, Fuzhou Beihai, Beijing Daxing Liancheng, Nanjing Jakarta, etc. Air China plans to increase the number of flights on more than 10 routes, including Beijing Warsaw, Milan, and Budapest, and add two international routes, Beijing Daxing Frankfurt and Beijing Daxing Milan. According to data from China Eastern Airlines, the average weekly planned departure frequency for its international and regional routes is 1400.

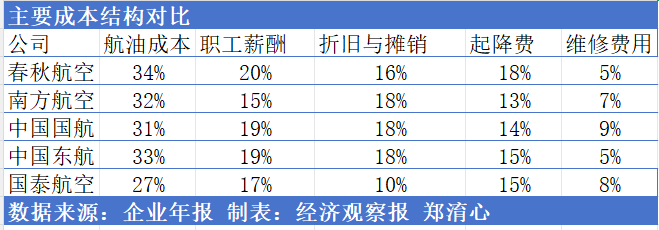

In addition to improving efficiency, aviation fuel - as the largest component of an airline's total operating costs, its price fluctuations also directly affect the airline's profitability.

In 2025, benefiting from the decrease in aviation fuel prices, the aviation fuel costs of Air China, China Eastern Airlines, and China Southern Airlines were 50.041 billion yuan, 43.69 billion yuan, and 52.526 billion yuan, respectively, a year-on-year decrease of 6.85%, 3.98%, and 4.48%. But starting from March 2026, the Middle East conflict will lead to an increase in fuel costs, which may raise the operating costs of airlines.

Air China once pointed out in its financial report that if the average aviation fuel price increases or decreases by 5% while keeping other variables constant, the cost of the group's aviation fuel will increase or decrease by approximately 2.502 billion yuan. China Southern Airlines' calculation level is comparable to that of Air China. If fuel prices rise or fall by 10%, it will result in an increase or decrease of 5.253 billion yuan in operating costs during the reporting period.

In response, China's civil aviation has uniformly increased the fuel surcharge for domestic routes, with a charge of 60 yuan per passenger for segments below 800 kilometers (inclusive) and 120 yuan for segments above 800 kilometers, which is five times higher than the previous standard.

Faced with the rise in oil prices, Wu Chenyue said that airlines can take proactive measures to optimize flights, explore new measures such as fuel control and conservation; Raising the fuel surcharge can only partially share the cost. The original intention of designing fuel surcharges is to have airlines bear no less than 20% of the additional costs, with passengers bearing the remaining portion. But the actual coverage ratio depends on demand. A high occupancy rate results in a high coverage ratio; If the demand is not good and the number of passengers decreases, the coverage ratio will decrease. Therefore, the actual impact of oil prices depends on the duration of high oil prices, actual demand, and the airline's ability to adjust bare ticket prices.

Cook hands over the baton, Apple's new CEO is confirmed, and the "hardware soul" of the 4 trillion yuan empire takes over

Volkswagen launches three new energy vehicles in China, AURA and ERA, with "twin" English names. Industry suggests more recognizable Chinese names. Volkswagen responds: There are no plans to change Chinese names for the new cars

Did humans lose? The humanoid robot Half Horse won the championship with 50 points, and behind it is the ultimate test before mass production

Subscribe

Subscribe