2026-04-13 16:03

![]()

When the commercial vehicle industry faced demand differentiation and cost pressure, Yutong Bus (600066. SH) submitted an "alternative" financial report.

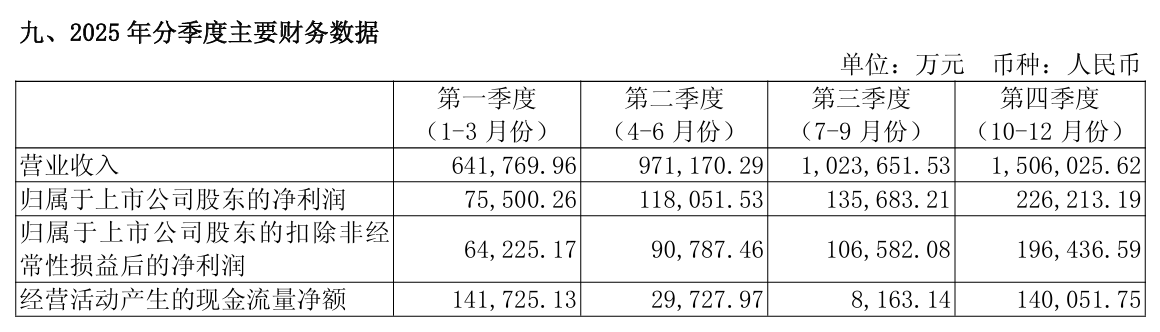

In 2025, Yutong Bus's revenue was 41.426 billion yuan, with a net profit attributable to the parent company of 5.554 billion yuan, a year-on-year increase of 34.94%. More worth exploring than the numbers are the financial structure and business logic that support its growth: a return on equity (ROE) of up to 38.03%, the proportion of overseas revenue exceeding 50% for the first time, and interest bearing liabilities that have been zero for several consecutive years.

Behind these financial data lies the long-term value of restraint and deep cultivation of this leading bus company.

How to grow, more meaningful than growth itself

The figures in Yutong Bus's 2025 financial report are not surprising: it sold 49518 buses throughout the year, a year-on-year increase of 5.54%; Operating revenue was 41.426 billion yuan, a year-on-year increase of 11.31%; The net profit attributable to shareholders of the listed company was 5.554 billion yuan, a year-on-year increase of 34.94%.

In 2025, when the commercial vehicle industry is under overall pressure and demand is structurally differentiated, such growth is already not easy. But what is more worth questioning than the growth figures is: where does profit come from? Is it sustainable? Is the financial structure healthy?

An easily overlooked detail is the deduction of non attributable net profit. In 2025, Yutong's non attributable net profit was 4.58 billion yuan, a year-on-year increase of 32.05%. This growth rate is highly matched with the growth rate of net profit attributable to shareholders (34.94%), with a difference of only about 2.9 percentage points between the two.

What does this mean? In the A-share market, some companies' net profit growth may come from non recurring gains and losses such as government subsidies, asset disposal gains, or fair value changes. But Yutong does not belong to these situations. The vast majority of its profit growth is contributed by its main business, and non recurring gains and losses have minimal disturbance to profits, making its growth highly valuable.

In other words, Yutong's growth is not achieved through "reporting", but through selling cars, controlling costs, and improving efficiency.

Just looking at the absolute scale of revenue and profit is not enough to judge the quality of a company's operations. The more critical indicator is the change in profitability.

In terms of gross profit margin, Yutong's overall gross profit margin for the whole year of 2025 is 24.14%, an increase of 1.20 percentage points year-on-year. More noteworthy is the quarterly trend: the gross profit margin in the fourth quarter reached 27.26%, a year-on-year increase of 1.36 percentage points and a month on month increase of 3.28 percentage points.

The quarterly improvement in gross profit margin indicates that Yutong continues to make efforts in controlling raw material costs, optimizing product structure (especially increasing the proportion of high gross profit overseas vehicle models), and other aspects.

In terms of net profit margin, the annual net profit margin was 13.58%, an increase of 2.42 percentage points year-on-year. There is an important observation here: the increase in net profit margin (2.42 percentage points) is greater than the increase in gross profit margin (1.20 percentage points).

The difference between the two reflects the enhanced cost control capability of Yutong. With the expansion of sales scale, fixed costs such as management expenses and sales expenses are being diluted, and the economies of scale are continuing to be realized.

In terms of return on equity (ROE), the weighted average ROE for the whole year reached 38.03%, a significant increase of 7.09 percentage points year-on-year. 38.03% of ROE is at the top level in the A-share market, far exceeding the average of the commercial vehicle industry. ROE is a core indicator for measuring shareholder return ability, which indicates that Yutong's efficiency in creating profits through shareholder investment capital is extremely high.

If the income statement shows' how much was earned ', then the balance sheet reveals' whether it is healthy'.

At the end of 2025, Yutong's total assets were 32.99 billion yuan, total liabilities were 17.146 billion yuan, and the asset liability ratio was 51.97%, a significant decrease of 5.55 percentage points from 57.52% at the end of 2024. The continuous contraction of debt scale means that Yutong's debt repayment risk is further reduced.

But the most striking detail is the structure of the debt. According to the financial report disclosure, Yutong has no short-term borrowings, long-term borrowings, or payable bonds. That is to say, this enterprise with an annual revenue of over 40 billion yuan will maintain zero interest bearing liabilities for the long term.

In the commercial vehicle industry, this is extremely rare. Most companies will use financial leverage to expand their scale, and interest bearing debt is the norm. Yutong's choice is exactly the opposite: it does not rely on external borrowing and relies entirely on its own accumulated cash flow to support business expansion. The autonomy and composure of this financial management give the company great strategic flexibility when facing industry cycle fluctuations. Simply put, it means there is no need to look at the face of financial institutions or worry about repaying debts.

Of course, a lower asset liability ratio is not necessarily better. The level of 51.97% is considered by the company as a 'reasonable healthy range', which retains sufficient financial safety margins without being overly conservative and affecting capital efficiency.

The cash flow statement is often the most easily misread part by the outside world. In 2025, Yutong's net cash flow generated from operating activities was 3.197 billion yuan, a year-on-year decrease of 55.67%. Looking at this decrease alone, it is easy to raise concerns: Has it become difficult to collect payments? Has the quality of sales decreased?

However, this is not the case. The increase in cash outflows from Yutong's operating activities is mainly due to the company's abundant self owned funds. Therefore, on the basis of the original normal and healthy accounting period, in order to share the development achievements with the industry chain, it actively reduced the scale of accounts payable, resulting in an increase in cash outflows from operating activities. This measure will help maintain a good cooperative relationship between Yutong and its suppliers, and also contribute to the overall positive development of the bus industry chain.

Yutong's accounts receivable turnover and other indicators did not show any abnormal fluctuations. The fact that Yutong's operating cash flow has remained large and positive for several consecutive years is more convincing than the year-on-year fluctuations in a single year: Yutong has a sustained self generating ability, which can support an annual R&D investment of over 1.8 billion yuan and a global market layout.

In a financial structure with zero interest bearing liabilities, short-term fluctuations in cash flow do not have any directional debt repayment risk. This is more like a result of "active choice", where Yutong arranges funding expenditures based on business expansion needs, rather than passively responding to debt pressure.

The common direction of the above financial data is that Yutong Bus will not have complex capital operations or aggressive financial leverage in 2025, but will achieve high-quality and sustainable growth.

Can overseas turbulence and domestic stability coexist

In the 2025 annual report of Yutong, a number has symbolic significance: overseas sales revenue exceeded domestic business for the first time.

In 2025, Yutong's overseas sales revenue reached 21.108 billion yuan, a year-on-year increase of 38.87%. This growth rate far exceeds the overall revenue growth rate of the company (11.31%), becoming the core driving force behind the overall revenue growth.

More importantly, the proportion change: the proportion of overseas revenue to main business revenue has increased to 57.81%, surpassing domestic business for the first time. This is a milestone leap forward. It means that Yutong is no longer a bus company mainly focused on the Chinese market, but a truly global company.

Overseas business not only contributes revenue, but also contributes a higher proportion of profits. Data shows that the gross profit margin of overseas business is as high as 29.62%, while the gross profit margin of domestic business is 19.09%, a difference of 10.53 percentage points between the two. The increase in the proportion of high gross profit overseas business has directly driven the overall profitability of the company.

This gap reflects the competitive landscape of overseas markets and Yutong's own pricing ability. In overseas markets such as Europe, America, and the Middle East, Yutong did not win with a low price strategy, but entered a relatively high-end market segment with its comprehensive strength in technology, products, and services. With the continuous increase in the proportion of overseas revenue, there is still room for further improvement in the overall gross profit margin of the company.

From the perspective of sales volume, Yutong will export 17149 buses by 2025, a year-on-year increase of 22.49%. Yutong has achieved mass sales in more than 60 countries and regions worldwide, exporting over 130000 buses of various types.

In high-end European markets such as the UK, Norway, and the Netherlands, Yutong's new energy buses have achieved mass sales and are operating well. These markets have high entry barriers and strict customer requirements, and being able to stand firm is a validation of product and brand strength.

An easily overlooked but crucial change is the upgrade of overseas business models. Yutong has achieved localized cooperation through KD assembly in more than ten countries and regions, including Kazakhstan, Pakistan, and Ethiopia. This means that Yutong has completed the business model upgrade from product output to "technology output+brand authorization".

The advantage of this model is that, on the one hand, KD assembly can reduce tariff and logistics costs, and improve the price competitiveness of products; On the other hand, by deeply binding with local partners, trade barriers and geopolitical risks can be avoided to a certain extent. The successful experience of this model can be copied to other emerging markets.

Compared with the rapid development of overseas markets, the domestic bus market as a whole is facing greater pressure in 2025. The passenger transport market has experienced an overall decline due to changes in demand structure, with a year-on-year decrease of 13.01% in demand for large and medium-sized passenger cars.

Against the backdrop of the overall decline in the large and medium-sized passenger bus market, Yutong achieved a sales volume of 16500 vehicles throughout the year, a year-on-year decrease of 7.8%, which is more than 5 percentage points higher than the industry average. This means that during the downward cycle, Yutong not only did not collapse, but also further consolidated its leading position in the large and medium-sized passenger car market.

In terms of the public transportation market, benefiting from the dual benefits of the continuation of the "trade in" subsidy policy and the upgrading of environmental standards, the sales volume of large and medium-sized public transportation in China increased by 4.81% against the trend. Yutong seized this policy opportunity and sold 5631 large and medium-sized buses, a year-on-year increase of 8.6%, outperforming the market growth rate.

In the core track of new energy public transportation, Yutong's leading advantage continues to expand. The annual sales volume of new energy buses was 5549, a year-on-year increase of 7%, significantly exceeding the industry's average growth rate of 1.6%. According to Shanghai Securities News, in the school bus market, despite the overall shrinking demand, Yutong still won 49.7% of the market share with product quality and brand influence, firmly ranking first in the segmented market.

These market performances are not accidental. According to the annual report and related materials, Yutong's strategy in the domestic market can be summarized as "closely following market demand in research and development".

In the field of tourism passenger transportation, Yutong has captured the trend of upgrading tourism consumption - tourism is developing towards high-end and small group direction. For the high-end tourism market, Yutong has launched high-end models such as S12; In response to the trend of small group tours, the "Tianjun" series of light travelers has been launched. These products contributed significant sales in 2025.

In the public transportation market, facing the reality of declining passenger flow, Yutong believes that the industry trend is moving towards "miniaturization and aging". To this end, the company has developed new products such as ride hailing minibuses and low floor aging friendly buses, which accurately match the needs of urban micro circulation buses and elderly travel.

These product level layouts together form a "moat" for Yutong to resist industry downturns in the domestic market. When competitors were still fighting price wars for homogeneous products, Yutong found growth points through product differentiation.

Do we have to choose between research and profit

The growth of profits, breakthroughs in overseas markets, and consolidation of domestic barriers are the manifestations of Yutong's business performance at the financial and operational levels. The deeper question is: What are the long-term and systematic capabilities that support these achievements?

Yutong's annual report data and company business model provide two answers: one is continuous and efficient R&D investment, and the other is the difficult to replicate "three line model". The former builds a moat of technology and products, while the latter forms barriers to service and customer relationships.

In 2025, Yutong's R&D expenditure will be 1.808 billion yuan, accounting for 4.36% of its operating revenue. In the bus industry, this proportion is at a high level.

But more noteworthy than the scale of investment are two phenomena: one is that while maintaining high R&D investment, Yutong has achieved a high-speed growth of 34.94% in net profit attributable to its parent company; The second is to accurately convert R&D investment into quantifiable technological breakthroughs and product competitiveness.

A common logic in financial analysis is that when a company's profits decline, the reason is often attributed to "excessive R&D investment". But Yutong provides a counterexample - high R&D investment and high profit growth can coexist.

From the data, the R&D intensity (R&D expenditure/operating income) in 2025 will be 4.36%, while the net profit margin will increase to 13.58%, both of which are at a relatively high level. This means that Yutong's R&D investment is not cost consumption, but value creation, that is, R&D expenditures bring corresponding revenue growth and profit returns. Behind this is a high degree of alignment between research and development direction and market demand, as well as continuous optimization of research and development management efficiency.

According to the annual report and related materials, Yutong's R&D investment has achieved quantifiable breakthroughs in multiple core technology fields. In addition to technological breakthroughs, the direction of research and development investment is equally crucial.

The annual report shows that Yutong's research and development focus covers overseas high-end public transportation/tourism products, pure electric light passenger series, hydrogen fuel forward-looking technology, assisted driving systems, etc. These directions precisely align with the development trend of "electrification, high-end, and intelligence" in the global bus industry, and also provide sufficient technical ammunition for product iteration in the next 3 to 5 years.

If research and development is a manifestation of hard power, then the "three direct models" are the soft power barriers built by Yutong in its business model and service system. This model is one of Yutong's core advantages that distinguish it from its competitors.

The so-called "three direct sales" refer to direct sales, direct service, and direct financing. Among them, "direct sales" refers to shortening the reaction chain and getting closer to the market; Direct service "refers to direct services provided by manufacturers, with customer satisfaction as the assessment standard; Direct financing "refers to financial autonomy with zero interest bearing liabilities.

Traditional commercial vehicle companies generally adopt the dealer model - the OEM sells the car to dealers, who then sell it to end customers. The advantages of this model are light assets and fast expansion, but the disadvantage is that there are distributors between the host factory and end customers, making it difficult to timely transmit changes in market demand to the research and development and production ends.

Yutong adopts a direct sales model: the sales team faces customers directly without any intermediaries. This means that customer needs, pain points, and usage feedback can be transmitted to the company in the shortest possible chain, with fast response times and a more accurate and sensitive perception of the market.

In the commercial vehicle industry, after-sales service is usually undertaken by dealers or third-party service providers. Their profit model determines their service motivation: earning profits through maintenance and parts sales. This may lead to issues such as excessive maintenance and delayed response.

Yutong's direct service model is completely different: the service team is directly under the manufacturer, and the core of its performance evaluation is customer satisfaction. The company will commission a third-party organization to conduct a customer satisfaction survey every year, which includes indicators such as vehicle operation rate. The goal of the service team is to help customers' cars not break down, operate well, and make money, thereby encouraging them to repurchase.

This model will be further upgraded in 2025. Yutong has released the commercial vehicle service brand "Yu+Direct Service" covering the whole scene of "travel, logistics and operation", and made eight service commitments.

The support for this service brand lies in its global service network. By the end of 2025, Yutong has over 400 authorized service outlets in overseas markets, with an average service radius of 120 kilometers, covering all target markets overseas. In China, a guarantee system based on direct service has also been established.

Direct financing "in Yutong's model refers to providing financial support directly to customers, but it also reflects Yutong's own financial philosophy of not relying on external borrowing. Yutong has maintained zero interest bearing liabilities for a long time and relies entirely on operating cash flow to support its business development. This financial autonomy allows companies to operate their businesses with a true long-term perspective, without the need to make short-term decisions to cater to banks or bondholders.

The effect of the "three straight model" is not limited to the conceptual level, but is reflected in specific business results.

From financial data, Yutong has maintained a high gross profit margin despite the overall weak demand in the domestic market. This is partly due to the direct sales model reducing the profit sharing in intermediate links. At the same time, the high customer satisfaction brought by the direct service model translates into a higher repurchase rate and brand loyalty, which is particularly important in the B-end markets such as public transportation and passenger transport.

Reject misinterpretation and view the future in plain reality

Any analysis of a company's annual report cannot avoid making judgments about the future. For Yutong, the outlook section needs to be particularly cautious. The most appropriate way is to objectively sort out the visible opportunities and short-term fluctuations that need to be addressed in the future based on industry trends and the actual capabilities of the company.

In the first quarter of 2026, Yutong's sales performance was relatively average. But this is not an accident, it is a normal manifestation of the industry's seasonality.

The bus industry has obvious seasonal characteristics. Core sales and delivery are concentrated in the second half of each year, especially in the fourth quarter. This is because the procurement plans of customers such as bus companies and passenger transport enterprises are usually linked to annual budgets and government subsidy cycles, and the end of the year is the peak period for centralized delivery. Therefore, the first quarter is often the traditional off-season for the industry and does not represent the annual trend.

This seasonal pattern can also be traced in Yutong's historical data. The first quarter of 2025 was not the highest point of the year, but it ultimately achieved steady growth throughout the year. Therefore, for the sales performance in the first quarter of 2026, it should not be overly interpreted as a deterioration of fundamentals, but rather observed in the context of the entire year.

Despite the overall weak demand in the domestic traditional bus market, there are still multiple deterministic sources of incremental growth in the coming years, including the continued implementation of the "trade in" policy, the demand for vehicle replacement brought about by the upgrading of environmental standards, the rigid demand for vehicle aging adaptation, and the arrival of stock renewal cycles.

In 2025, the sales of large and medium-sized public transportation in China will benefit from the continuation of the "trade in" subsidy policy and the upgrading of environmental standards, achieving counter trend growth. According to relevant plans, this policy will continue to play a positive role in 2026 and subsequent years. The replacement process of new energy buses has not yet been completed, especially in third - and fourth tier cities and county markets, where there is still significant room for renewal.

It should be pointed out that Yutong's overseas business will surpass domestic revenue for the first time in 2025, but this does not mean that the growth of overseas markets has peaked. On the contrary, global bus electrification is still in its early stages.

Despite the rapid growth of new energy buses in regions such as Europe, Latin America, and the Middle East, the overall penetration rate is still relatively low. Traditional fuel powered buses still dominate the overseas ownership. With the establishment of carbon emission reduction targets in various countries and the promotion of public transportation electrification policies, there is a huge space for the replacement of new energy buses.

Certainty is the rarest value

In 2025, Yutong will not have dramatic counterattacks like some companies. Its market performance will be flat and stable. What the outside world sees is healthy cash flow, clean balance sheet, continuous R&D investment, and a difficult to imitate "three-way model". In a business environment full of uncertainty, this high-quality growth filled with "certainty" is precisely the greatest value that Yutong provides to investors and the industry.

Wen/Wang Ziyang

3M China President Ding Hongyu: 25 years on the same frequency as the times

AMD Senior Vice President and President of Greater China, Pan Xiaoming: Keenly Capturing the Pulse of China's Economic Development

Kong Na, Chairman and President of Angel Group: Supporting the Upgrading of the Real Economy to a Brand Economy