2026-04-09 11:35

![]()

In the past few years, everyone has been talking about 'bottom warehouse products'. Stable excess returns are the key to measuring 'bottom position products'. But we see that the excess returns of the vast majority of fund managers are not stable. ButHua'an Fund's Zhang Xu redefined the true "bottom position product" within a limited investment periodIn these six years, the market style and bull bear cycle have undergone a complete transition, which means that Zhang Xu's excess returns are a pure alpha, not relying on the style factor of smart beta.

Scarce 'bottom position' fund managers

Zhang Xu is a representative of the new generation of fund managers: born in the 1990s, first prize in the national high school physics competition, recommended for admission to the junior class of the University of Science and Technology of China, with a bachelor's and master's degree in statistics, and a representative of active quantification in public funds. He is a typical 'STEM man' with a very simple learning and professional experience, focusing on the field of quantification for a long time.

Zhang Xu's proactive quantification is different from what is commonly believed to be index enhancement. There may be a certain deviation in tracking error compared to the benchmark, but he is able to grasp the main line of the market every yearHe has a unique industry rotation model that selects configurations based on business prosperity across 5 to 7 industries. The ability of Zhang Xu to grasp the market mainline is reflected in the overallocation of consumer goods, pharmaceuticals, and electronics in 2020, new energy in 2021, non bank finance in 2022, TMT in 2023, banks in 2024, and upstream non-ferrous resources in 2025.

Many people believe that industry rotation cannot be a long-term effective investment framework, but Zhang Xu has proven the sustainability of this framework's excess returns. Through further disassembly, we can see that Zhang Xu's industry rotation is fundamentally different from the traditional meaning of rotation:

1) The traditional industry rotation relies entirely on subjective judgment, and the earliest macro cycle rotation began in the era of 4 trillion yuan. As macro fluctuations gradually decrease, this framework system becomes less effective. Zhang Xu's industry rotation is quantitatively driven, fully leveraging the breadth advantage of quantitative investment;

2) The traditional industry rotation is basically all in one or two industries, betting on the right ranking at the top and betting on the wrong ranking at the bottom. This approach has a clear win rate issue. Zhang Xu's industry rotation will be based on the weight of each industry in the benchmark, with a certain deviation between over allocation and under allocation, without relying on one or two industries to overcome the market through over allocation.

Of course, Zhang Xu's ability to continue to outperform the market is definitely not achieved through a single move. In addition to industry rotation, Zhang Xu also has a multi factor stock selection approach that combines proactive and quantitative methods, and a systematic investment process. He is also one of the early active quantitative fund managers in the industry to adopt AI.

Zhang Xu cracked the "password" of the market

A fund manager's investment framework system will continue to iterate, but their underlying ideas are difficult to change. To truly understand how Zhang Xu overcame the market, we must understand the underlying logic of his investment. At the recent Spring Strategy Meeting of Open Source Securities, Zhang Xu shared his investment philosophy.

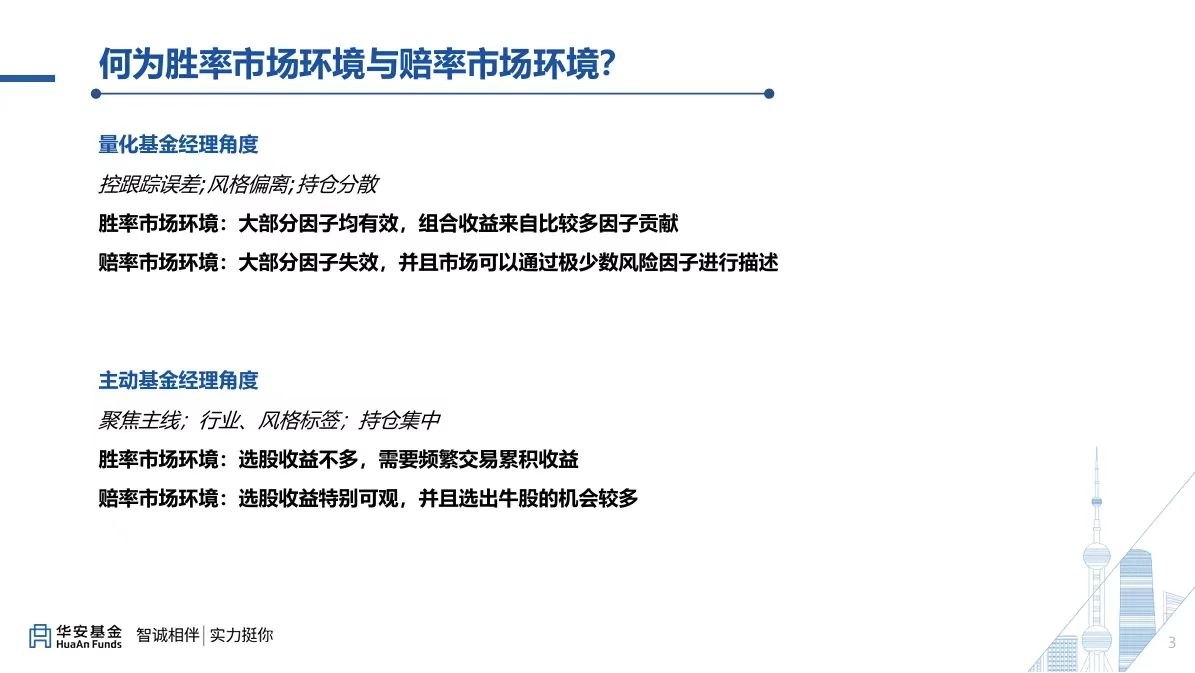

He divided the A-share market into two major environments: those with a higher winning rate and those with higher odds. From the perspective of quantitative fund managers, in a market environment where the winning rate is dominant, most factors are relatively effective and have high stability. In a market environment with favorable odds, most factors fail, and excess returns can only rely on the contribution of a very small number of factors.

From the perspective of active fund managers, in a market environment where the winning rate is dominant, excess returns are difficult to be contributed by a few bull stocks, and it is more necessary to defeat the market through certain trades. In a market environment with favorable odds, relying on a few bull stocks can contribute the main excess returns.

Zhang Xu divided the A-share market based on different winning rates and odds environments. The typical winning environment is in the first half of 2020, before the Spring Festival to the second quarter of 2022, and in the second and third quarters of 2024. The typical environments with favorable odds are the third quarter of 2020, the first quarter of 2023, and the second quarter of 2025. In an environment where the winning rate is dominant, it is necessary to rely on rotation to overcome the market; In an environment with favorable odds, it is necessary to rely on stock selection to overcome the market.From the comparison of performance, under the winning rate environment, the index has strengthened and won, while under the odds environment, Wande has a mixed advantage in the biased stock market.

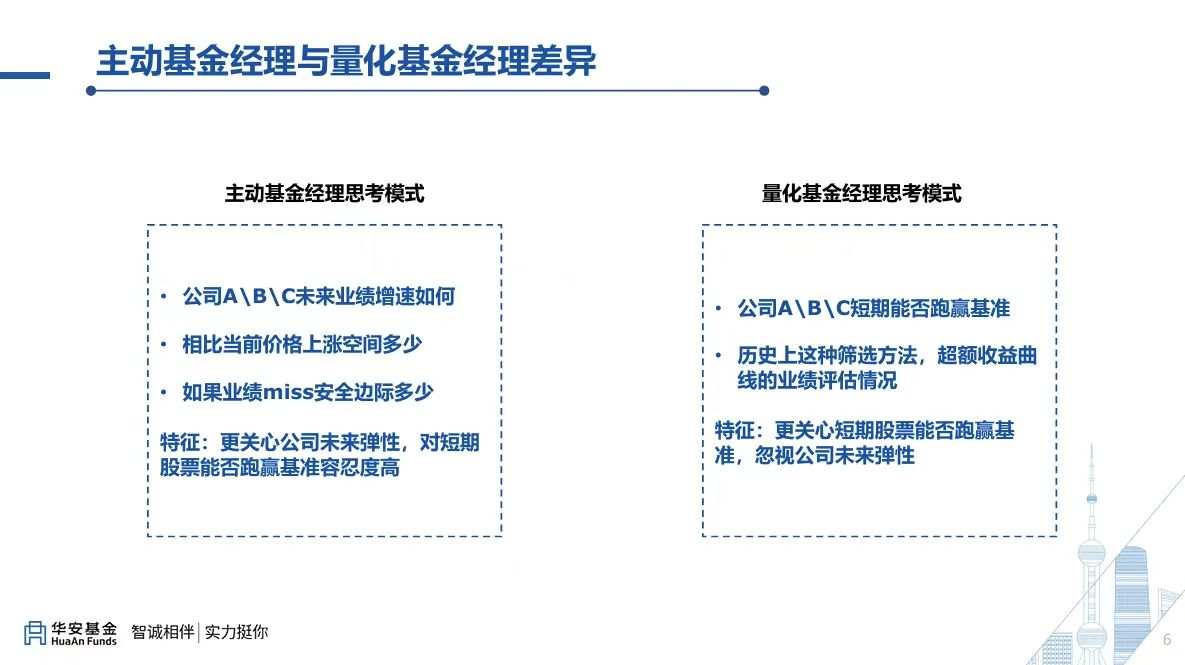

In Zhang Xu's view, actively selecting stocks is more of an odds thinking approach, where fund managers deduce the potential space of the stock from fundamental analysis, but do not care about whether it can outperform the market in the next month. Quantitative fund managers are more of a winning rate mindset, with the goal of achieving a higher monthly winning rate.

Simply put,When Zhang Xu is making investments, he will first see clearly what cards the market environment is playingIn a volatile environment where the winning rate is dominant, it is more advantageous to adopt a strategy of quantitative investment diversification and rely on certain rounds to win. At this time, the market prefers defensive and rotational factors such as reversals, low volatility, and high dividends. In a market environment with favorable odds, it is more conducive to subjective stock selection with concentrated portfolio, and to win by grasping the main line of stock selection. At this point, the market prefers aggressive factors such as Beta, growth, market value, and analyst expectations.

The stock market is like a football game, with a "home and away system". Sometimes it is the "home field" for proactive stock selection, and sometimes it is the "home field" for quantitative investment. After understanding the environment, Zhang Xu will decide on his own coping strategy. This set of thinking framework reflects the comprehensiveness of Zhang Xu's proactive quantitative investment. That is, he can not only outperform in markets suitable for quantification, but also in markets suitable for active stock selection.

Specifically, when the market is in an odds environment where active stock selection dominates,Zhang Xu's problem-solving approach is to quantitatively replicate the alpha of active stock selection.Since active fund managers rely on "grasping the main line and researching the track" to make money in the odds environment, quantification can also introduce "odds based models". From past practice, Zhang Xu's industry allocation model can achieve a win rate of around 60%, but their odds can even reach 1.2 to 1.8.

Under the underlying concept of combining win rate and odds, Zhang Xu has formed a truly active quantification framework.When actively dominant, replicate the active alpha; When quantification is dominant, use the advantages of quantification.This underlying thinking is the key to Zhang Xu achieving a 100% annual win rate.

The rise of proactive quantification deserves attention

With the rapid popularization of AI, quantification has become the mainstream of the A-share market. In the field of private equity, quantifying the scale of private equity management has surpassed active investment and become the main price setter in the market. In public funds, active quantification relying on product stability and system scalability has become a rapidly rising force.

Of course, Zhang Xu's performance cannot be achieved without the strong platform empowerment of Hua'an Fund. According to the fund performance ranking of Guotai Haitong,Hua'an Fund's active equity performance in the past five years ranked first among 13 "equity large fund companies", and ranked second in the past seven years(Data source: Guotai Haitong - Fund Quarterly Report - Fund Company Equity and Fixed Income Asset Performance Ranking (20260102) - Fund Company Equity Fund Performance Evaluation); Data as of December 31, 2025.

Zhang Xu's new product, Hua'an Zhiyou Quantitative Stock Selection (Class A: 026859; Class C: 026866) is currently being released, which is a product that fully embodies Zhang Xu's "bottom warehouse" style.In 2026, Zhang Xu is still continuing to write his story.

The following data source: Fund Regular Report, as of December 31, 2025. The annual performance of all products managed by Zhang Xu in the past 5 years is as follows: Hua'an CSI 500 Index Enhancement A: Established on May 24, 2022, the performance benchmark is CSI 500 Index yield x 95%+bank current deposit interest rate (after tax) x 5%. The performance of this fund from May 24, 2022 to the end of the year (and performance benchmark), and the annual performance from 2023 to 2025 (and performance benchmark) were -5.16% (-1.60%), -12.32% (-7.03%), 3.74% (5.24%), and 33.05% (28.81%).Previous fund managers: Ma Tao (20220524-20251012), Zhu Baochen (20220530-20230706), Zhang Xu (20251013 present). Hua'an CSI 500 Index Enhancement C: Established on May 24, 2022, with a performance benchmark of CSI 500 Index yield x 95%+bank current deposit interest rate (after tax) x 5%. The performance of this fund from May 24, 2022 to the end of the year (and performance benchmark), and the annual performance from 2023 to 2025 (and performance benchmark) were -5.39% (-1.60%), -12.66% (-7.03%), 3.30% (5.24%), and 32.52% (28.81%). Previous fund managers: Ma Tao (20220524-20251012), Zhu Baochen (20220530-20230706), Zhang Xu (20251013 present). Hua'an CSI 1000 Index Enhancement A: Established on July 12, 2022, with a performance benchmark of CSI 1000 Index yield x 95%+bank current deposit interest rate (after tax) x 5%. The annual performance (and performance benchmark) of this fund from 2023 to 2025 is -3.52% (-5.95%), -2.76% (1.41%), and 28.77% (26.12%). From July 12, 2022 to the end of the year, less than half a year has passed, therefore performance will not be disclosed. Previous fund managers: Ma Tao (20220712-20251012), Zhu Baochen (20220801-20230706), Zhang Xu (20251013 present). Hua'an CSI 1000 Index Enhancement C: Established on July 12, 2022, with a performance benchmark of CSI 1000 Index yield x 95%+bank current deposit interest rate (after tax) x 5%. The annual performance (and performance benchmark) of this fund from 2023 to 2025 is -3.89% (-5.95%), -3.16% (1.41%), and 28.26% (26.12%). From July 12, 2022 to the end of the year, less than half a year has passed, therefore performance will not be disclosed. Previous fund managers: Ma Tao (20220712-20251012), Zhu Baochen (20220801-20230706), Zhang Xu (20251013 present). Hua'an Event Driven Quantitative Hybrid A: Founded on December 14, 2016, the performance benchmark is CSI 800 index yield * 75%+China bond total index yield * 25%.The annual performance (and performance benchmark) of this fund from 2021 to 2025 is 30.84% (0.00%), -17.86% (-15.94%), -8.63% (-7.36%), 21.82% (10.51%), and 38.06% (14.92%). Previous fund managers: Niu Yong (20161214-20180114), Sun Chenjin (20161219-20210117), Zhang Xu (20200518 present). Hua'an Event Driven Quantitative Hybrid C: Founded on March 20, 2023, the performance benchmark is the yield of CSI 800 index * 75%+the yield of China's total bond index * 25%. The performance (and performance benchmark) from March 20, 2023 to the end of the year, as well as the annual performance (and performance benchmark) for 2024 and 2025, were -13.34% (-9.01%), 21.20% (10.51%), and 37.42% (14.92%). Former fund manager: Zhang Xu (20230320 present). Hua'an China A-share Enhanced Index: Established on November 8, 2002, with a performance benchmark of 95% * MSCI China A-share Index yield+5% * financial interbank deposit interest rate. The annual performance (and performance benchmark) of this fund from 2021 to 2025 is 5.58% (0.00%), -22.83% (-20.94%), -14.06% (-11.03%), 4.99% (11.50%), and 21.04% (20.52%). Previous fund managers: Liu Xinyong, Yin Mizhi (20021108-20030917), Wang Guowei (20030918-20050524), Liu Guanghua (20050525-200080424), Liu Guanghua, Liu Ying, Xu Zhiyan (20080425-20081010), Liu Ying, Xu Zhiyan (20081011-20100625), Xu Zhiyan (20100626-20100901), Xu Zhiyan, Niu Yong (20100902-20121221), Niu Yong (20121222-20171224), Niu Yong, Xu Zhiyan (20171225-20180114), Xu Zhiyan, Ma Tao (20180115-20250105) Ma Tao (20250106-20250720),Zhang Xu (20250721-20260301), Zhang Xu, Ouyang Jun (20260302 present). Hua'an CSI 300 Enhanced A: Established on September 27, 2013, the performance benchmark is 95% x CSI 300 index yield+5% x post tax current deposit benchmark interest rate of commercial banks during the same period. The annual performance (and performance benchmark) of this fund from 2021 to 2025 is 1.56% (-4.92%), -19.91% (-20.53%), -13.44% (-10.79%), 15.14% (14.04%), and 23.10% (16.79%). Previous fund managers: Dong Liang (20130927-20141229), Niu Yong (20141230-2015.0120), Niu Yong Xie Dongxu (20150121-2017125), Niu Yong (20170126-20171224), Niu Yong, Xu Zhiyan, Sun Chenjin (20171225-20180114), Xu Zhiyan, Sun Chenjin (20180115-20210117), Xu Zhiyan, Zhang Xu (20210118-20250105), Zhang Xu (20250106 present). Hua'an CSI 300 Enhanced C: was established on September 27, 2013, with a performance benchmark of 95% x CSI 300 index yield+5% x post tax current deposit benchmark interest rate of commercial banks during the same period. The annual performance (and performance benchmark) of this fund from 2021 to 2025 is 1.16% (-4.92%), -20.23% (-20.53%), -13.78% (-10.79%), 14.68% (14.04%), and 22.62% (16.79%). Previous fund managers: Dong Liang (20130927-20141229), Niu Yong (20141230-2015.0120), Niu Yong Xie Dongxu (20150121-2017125), Niu Yong (20170126-20171224), Niu Yong, Xu Zhiyan, Sun Chenjin (20171225-20180114), Xu Zhiyan, Sun Chenjin (20180115-20210117), Xu Zhiyan, Zhang Xu (20210118-20250105), Zhang Xu (20250106 present).Hua'an CSI 300 Enhanced Strategy ETF: Established on December 21, 2022, with performance benchmark based on the returns of the CSI 300 Index. The annual performance (and performance benchmark) of this fund from 2023 to 2025 is -9.56% (-11.38%), 20.85% (14.68%), and 18.52% (17.66%). Previous fund managers: Xu Zhiyan, Zhang Xu (20221221-20250629), Zhang Xu, Wang Chao (20250630 present). Hua'an CSI 300 Enhanced Strategy ETF Initiated Connect A: Established on June 17, 2025, with performance benchmark based on the returns of the CSI 300 Index. The performance (and benchmark) of this fund from June 17, 2025 to the end of the year was 15.60% (18.50%). Previous fund managers: Xu Zhiyan, Zhang Xu (20250617 present). Hua'an CSI 300 Enhanced Strategy ETF Initiated Connect C: Established on June 17, 2025, with performance benchmark based on the returns of the CSI 300 Index. The performance (and benchmark) of this fund from June 17, 2025 to the end of the year was 15.49% (18.50%). Previous fund managers: Xu Zhiyan, Zhang Xu (20250617 present). Hua'an CSI A500 Enhanced Strategy ETF: Established on June 18, 2025, with performance benchmark based on the CSI A500 Index yield. The performance (and benchmark) of this fund from June 18, 2025 to the end of the year was 17.61% (24.37%). Previous fund managers: Zhang Xu, Wang Chao (20250618 present). Hua'an CSI A500 Enhanced Strategy ETF Initiated Connection A/C: Established on August 11, 2025, with a performance benchmark of CSI A500 Index yield x 95%+bank current deposit interest rate (after tax) x 5%. A/C shares will not disclose their performance within half a year from their establishment until the end of 2025.

Note: According to the latest prospectus, the current charging standards for subscription fees, redemption fees, and sales service fees of this fund are as follows (rate discounts are subject to display by sales institutions; M/N refers to the amount/holding period respectively): The subscription rate for Class A shares is 0.80% for M<5 million yuan; M ? 5 million yuan, 1000 yuan/transaction (investors charge subscription/purchase fees for A-class fund shares through sales agencies, and no subscription/purchase fees for A-class fund shares through fund managers), no sales service fees will be charged; Class C shares do not charge subscription fees, and the sales service fee rate is 040% per year (sales service fee applies to Class C fund shares subscribed/subscribed by investors through sales agencies and held for a continuous period of no more than one year). The sales service fees charged by investors for subscribing/purchasing Class C fund shares through the manager shall be returned to investors along with the redemption proceeds (or liquidation proceeds) when the investors redeem the fund shares (including conversion and transfer, the same below) or terminate the fund contract; Investors who subscribe/purchase Class C fund shares through sales agencies will receive sales service fees for fund shares held for more than one year. When the investor redeems the fund shares or terminates the fund contract, the fees will be returned to the investor along with the redemption proceeds (or liquidation funds). A. The redemption rate for Class C shares is 1.50% for N<7 days; 7 days ? N<30 days 1.0%; 30 days ? N<180 days 0.5%; N ? 180 days 0.00%; The management fee rate is 1.20% per year; The hosting fee is 0.20% per year.

Risk Warning: The above content only represents the views at that time and may change in the future. It is for reference only and does not constitute any investment advice or guarantee. Please refer to product legal documents such as fund contracts, fund prospectuses, and fund product information summaries for investment strategies. Fund management companies do not guarantee a certain profit, nor do they guarantee a minimum return. The past performance of a fund does not predict its future performance, and the performance of other funds managed by the fund manager does not constitute a guarantee of fund performance. This fund is an equity fund with expected returns and expected risk levels higher than hybrid funds, bond funds, and money market funds. If this fund invests in the underlying stocks of the Hong Kong Stock Connect, it shall bear the unique risks arising from differences in investment environment, investment targets, market systems, and trading rules under the Hong Kong Stock Connect mechanism. Please carefully read the fund contract, prospectus and other legal documents of this fund for details. Funds carry risks and investments need to be cautious. This product is issued and managed by Hua'an Fund, and the sales agency is not responsible for the investment and redemption of the product.

Jiushi Intelligent CEO Kong Qi: Jingguan has always adhered to its original intention with rationality and interpreted the future with depth

Founder and CEO of Black Sesame Intelligence: Witnessing the Growth and Transformation of China's Economy through Economic Observation

White Rhino Autonomous Driving CEO Huang Gang: Jingguan injects new imagination and vitality into the high-quality development of China's economy