Economic Observer Follow

2026-04-01 21:42

![]()

On March 31, 2026, Everbright Bank (601818. SH/6818. HK) disclosed its 2025 annual report card.

According to the annual report, in 2025, Everbright Bank achieved a revenue of 126.311 billion yuan, a year-on-year decrease of 6.72%; The net profit attributable to the shareholders of the bank (hereinafter referred to as "net profit") was 38.826 billion yuan, a year-on-year decrease of 6.88%. As of the end of 2025, the total assets of Everbright Bank reached 71653.19 billion yuan, an increase of 2.96% compared to the end of the previous year.

On the afternoon of March 31st, Hao Cheng, the President of Everbright Bank, stated at the bank's 2025 annual performance meeting that Everbright Bank places effective improvement in quality in a more prominent position, not only focusing on scale, speed, and ranking, but also optimizing asset structure in key areas and tracks, enhancing the ability to expand customers in batches and import source funds, and promoting steady growth in asset liability scale.

Responding to pressure on revenue and net profit

Observing the annual performance trend of Everbright Bank in 2025, it can be found that the decline mainly occurred in the second half of 2025. According to the semi annual report of Everbright Bank, in the first half of 2025, the bank's revenue decreased by 5.57% year-on-year, but its net profit slightly increased by 135 million yuan year-on-year. By the third quarter, revenue continued to decline, and the growth rate of net profit experienced a reversal from positive to negative, with a year-on-year decrease of 10.99%. The net profit for a single quarter was 12.396 billion yuan. In the fourth quarter, the bank's net profit for a single quarter was only 1.808 billion yuan.

Breaking down the financial report, it was found that the decline in net profit of Everbright Bank in 2025 mainly comes from two aspects: first, the net interest income was 92.101 billion yuan, a year-on-year decrease of 4.565 billion yuan, a decrease of 4.72%; Secondly, other non interest income was 13.958 billion yuan, a year-on-year decrease of 5.72 billion yuan.

At the performance meeting, Liu Yan, Vice President and Chief Financial Officer of Everbright Bank, stated that in recent years, the banking industry has faced operational pressures such as a narrowing net interest margin and a decrease in intermediate income, due to policies such as the reduction of loan market quoted interest rates (LPR) and fee reductions. As a result, revenue growth has generally slowed down.

Liu Yan stated that based on the situation of Everbright Bank, the bank's negative revenue growth in 2025 is mainly affected by the following factors: firstly, the net interest margin has narrowed. Since 2024, the LPR interest rate has been lowered, coupled with the adjustment of existing housing loan interest rates. In 2025, the loan yield of the bank has been affected, while the downward pace of deposit interest rates is slower than that of loans. The net interest margin has narrowed year-on-year, which has constrained the growth of interest income; The second is a phased decline in other income. In 2024, the bond market interest rates experienced a significant decline, and the bank's investment asset valuation had a relatively high floating profit base. However, in 2025, the overall bond market interest rates rose, resulting in a certain floating loss in the bank's investment asset valuation, leading to a decrease in other income; The third is to coordinate development and security.The bank has increased its efforts to resolve related business risks and transform its operations, resulting in temporary pressure on credit card interest and fee income, which has had a certain impact on the growth of interest and fee income throughout the bank. Along with the decline in revenue, Everbright Bank has eased the downward pressure on profits by strengthening cost control, resulting in an 8.9% decrease in annual operating expenses, which is greater than the decline in revenue.

Liu Yan stated that 2026 is a year for Everbright Bank to solidify its foundation. Everbright Bank will adhere to differentiated development, create distinctive advantages, increase revenue, control costs, strengthen wind control, increase relevant resource support, and promote the stabilization and recovery of profitability.

Control Asset Quality

By 2025, Everbright Bank's total assets will exceed 7 trillion yuan. Among them, the total loan amount was 3.98 trillion yuan, an increase of 46.316 billion yuan or 1.18% from the end of the previous year.

Everbright Bank has outstanding achievements in technology loans and green loans. Among them, the balance of technology loans was 703.723 billion yuan, an increase of 64.985 billion yuan or 10.17% from the end of the previous year; The balance of green loans (new caliber) was 469.078 billion yuan, an increase of 56.048 billion yuan or 13.57% from the end of the previous year.

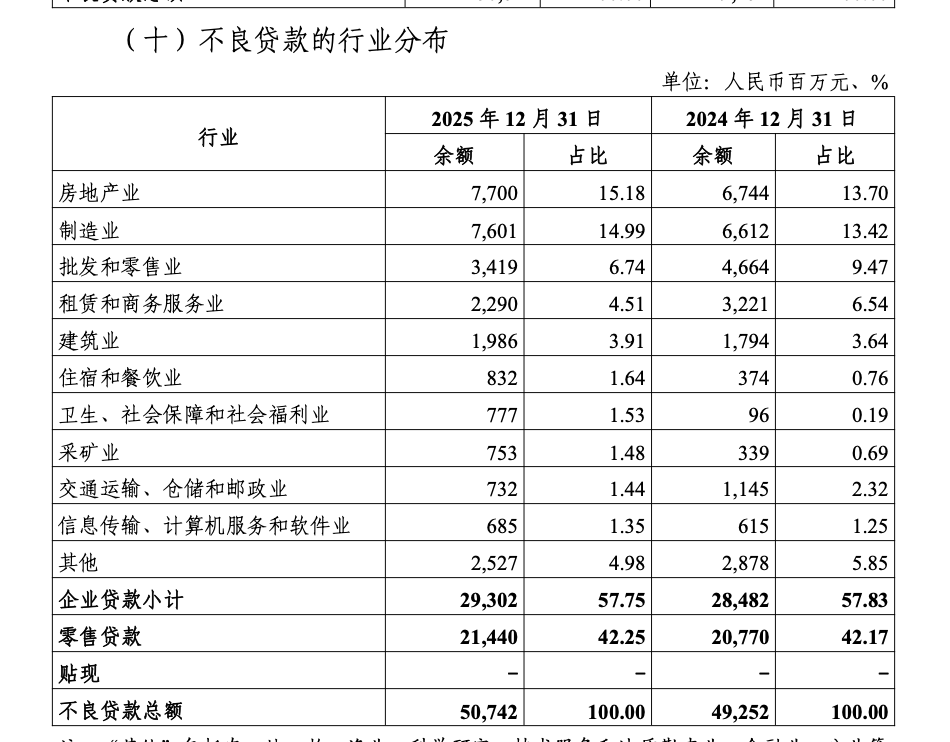

However, the asset quality of Everbright Bank is still under pressure. In 2025, the non-performing loans of Everbright Bank will continue to increase. As of the end of 2025, the bank's non-performing loan balance reached 50.742 billion yuan, an increase of 1.49 billion yuan from the end of the previous year; The non-performing loan ratio was 1.27%, an increase of 0.02 percentage points from the end of the previous year, and the overdue loan ratio was 2.13%, an increase of 0.11 percentage points from the end of the previous year.

From the perspective of non-performing loan industries, real estate still has the highest proportion. In 2025, the balance of non-performing loans in the real estate sector of the bank will be 7.7 billion yuan, accounting for 15.18%, an increase of 1.48 percentage points compared to 2024. The balance of non-performing loans in the wholesale and retail industry decreased by 1.245 billion yuan, while the balance of non-performing loans in the accommodation and catering industry increased from 374 million yuan in 2024 to 832 million yuan.

Qi Ye, Vice President of Everbright Bank, stated at the performance meeting that based on the new occurrence of non-performing loans, the overall scale of non-performing loans in the corporate sector has decreased compared to the previous year. In 2025, the bank will increase the risk clearance of real estate stock, smoothly and orderly promote platform based bonds, and implement non repayable loan renewals for small and medium-sized enterprises; In terms of retail loans, the quality of housing loans and consumer credit assets mainly based on credit cards is under pressure. The bank has identified them as key areas, established dedicated teams, mechanisms, tilted resources, and taken multiple measures to strengthen control and resolution. Positive results have also been achieved in 2025.

It is worth noting that in terms of credit cards, in 2025, Everbright Bank will shift its credit card business from direct operation to localized operation, that is, credit card business will return to branches.

Qi Ye stated that by 2025, the bank will fully mobilize the strength of its branches, deeply cultivate consumer scenarios, and accelerate structural optimization centered on satisfactory customers. In terms of risk governance, we adhere to strict control of new additions and resolution of existing ones, revise core approval policies, continuously optimize risk control models, strengthen refined management of existing customers and pressure reduction of potential high-risk customers, and enhance post loan collection efficiency. In the past year, the occurrence of credit card non-performing loans has remained stable with a slight decrease, and preliminary results have been achieved in risk management. The governance achievements of this year have strengthened the bank's confidence in the stability and improvement of its asset quality, and laid the foundation for future development.

The robot rental market has exploded, and by 2026, the scale of China's robot rental market will exceed 10 billion yuan

Ministry of Education: Compulsory education schools strictly prohibit the establishment of key classes, experimental classes, and fast/slow classes

The US electric vehicle market is experiencing a downturn. Car companies: The trend towards electrification will not change

Subscribe

Subscribe